Published 10 June 2025

Disputes with trading partners have significantly reduced external demand for Chinese products, underscoring China’s need to pivot toward domestic demand as a primary growth driver. But boosting domestic consumption is not merely a policy imperative for Beijing — it entails complete societal transformation that requires an integrated approach involving fiscal and monetary reform, structural changes to the economy, and cultural shifts in consumption behavior.

China’s imbalanced economic structure has been notorious for its low domestic consumption and overreliance on export and investment. Despite repeated stimulus efforts by the government, domestic consumption has not significantly expanded as intended.

Government stimulus fails to expand consumption

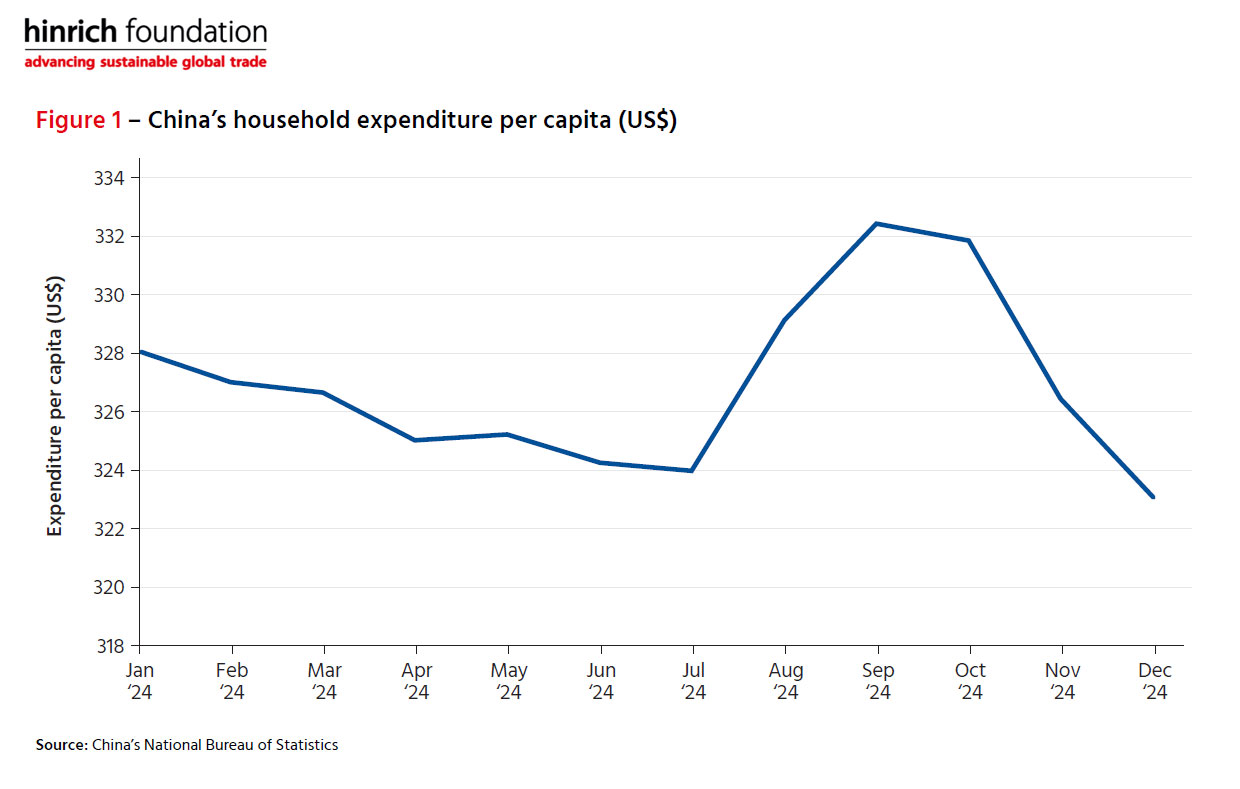

In September 2024, China announced an economic stimulus package totaling 12 trillion yuan (US$1.65 trillion). While the stimulus made some progress in addressing off-balance-sheet debt, it has proven insufficient to kickstart economic recovery. Officially, local government debt has nearly doubled since 2019, rising from 21.3 trillion yuan to 40.7 trillion yuan at the end of 2023. Besides its underwhelming scale as compared to the package implemented by the US in response to the pandemic, the Chinese stimulus disappointed as there has been no direct fiscal injection into the real economy. As a result, the stimulus has failed to expand China’s household consumption, which peaked in September 2024 and then dropped to a new low in the year.

Download China’s consumption dilemma in the age of Trump by Chen Gang:

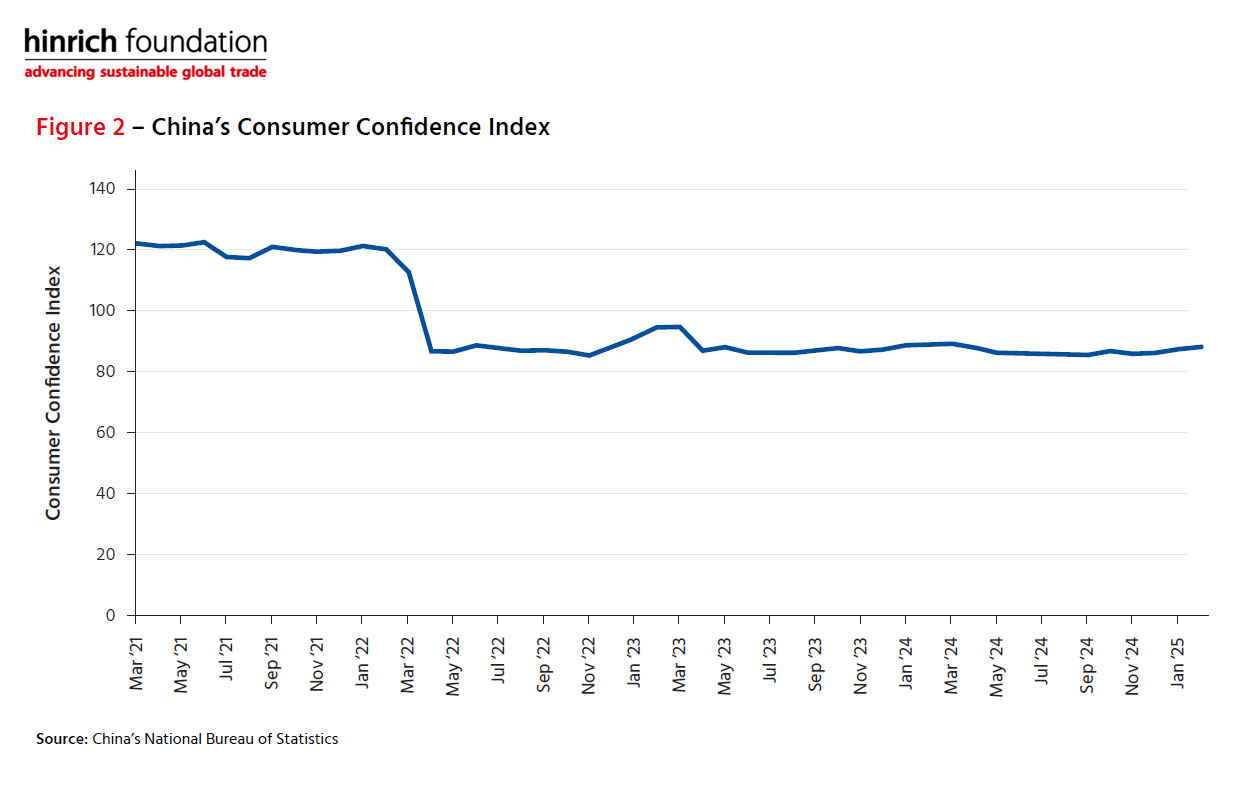

If the Chinese government is serious about consumption expansion, the policymakers need to review the effectiveness of the stimulus measures they’ve taken, which still largely support supply-side activity and investment-led growth, rather than directly targeting consumer confidence or purchasing power. In contrast to the 500-billion-yuan fund Beijing planned to raise to re-capitalize major state banks this year, the government raised the monthly minimum pension by only 20 yuan (US$2.78) to 143 yuan (US$19.85). Consumer sentiment remains cautious due to high youth unemployment and underemployment, a cascading effect from shrinking property wealth and a shift in savings behavior in uncertain times.

Confusing policy signals

In March 2025, a Party-wide austerity campaign was reintroduced with the intent of curbing bureaucratic extravagance and reinforcing Party discipline, but it also suppressed government-related consumption. The campaign prohibits lavish banquets, luxury travel, and opulent office environments — symbolic of official decadence — but these activities also constitute a significant portion of service-sector demand. In past austerity waves, notably in 2013–2014, sales at high-end restaurants, of luxury goods, and of premium alcohol brands plummeted. The 2025 relaunch is already generating similar behavioral shifts, with public institutions slashing entertainment budgets and officials avoiding conspicuous consumption altogether.

This restraint has a psychological and economic ripple effect beyond the state sector. Chinese consumers often take cues from elite behavior. When Party officials downplay materialism, middle-class citizens are also scaling back spending — particularly on discretionary items such as dining out, travel, or branded goods. The public spending cuts have a significant trickle-down effect on residents’ income and consumption, suppressing revenues of businesses that rely on government procurement and spending. The number of restaurants that closed down hit a record high nationwide, approaching 3 million in 2024. In first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, the monthly restaurant closure rates sometimes exceed 15%.

Deflation overshadows consumption prospect

China’s ongoing deflation poses a serious obstacle to its strategy of shifting toward a consumption-driven economy. The Chinese government has lowered the targeted consumer price index (CPI) increase from 3% to 2% in 2025, sending a clear policy signal that the government is becoming more tolerant of low inflation. But even the 2% target seems to be overoptimistic. The CPI, after stagnating in the preceding months, fell by 0.7% and 0.1% year-on-year in February and March 2025. While part of the decline was attributed to temporary factors, such as a favorable base effect from the 2024 Spring Festival and a drop in food prices due to good weather, the broader trend highlights systemic weaknesses in consumer demand.

In the shadow of President Trump’s high tariffs, China’s Producer Price Index (PPI), which tracks prices at the factory gate, underscores the depth of the deflationary cycle. In February and March 2025, the PPI in the industrial sector dropped by 2.2% and 2.5% year-on-year, marking the 30th month of negative PPI since October 2022. This suggests that industrial firms continue to face weak demand and are cutting prices to compete in a sluggish market. Persistent PPI deflation, a harbinger of CPI drop, reduces profitability, discourages capital investment, and increases financial pressure on firms already burdened by debt and overcapacity.

This industrial slowdown feeds back into the labor market. The urban jobless rate for 16-to-24-year-olds, excluding university students, was as high as 16.5% in March 2025, while the unemployment rate for 25-29-year-olds and 30-59-year-olds reached 7.2% and 4.1%. The official jobless rate, which does not account for job seekers who have given up on finding work or those located in rural China, is believed to seriously underestimate the dire reality.

Deflation also aggregates debt burdens in real terms, with highly leveraged real estate industry, local governments, and individuals facing higher default risks. Personal and household debts, especially among owners of small businesses, have become more prevalent in the ongoing economic downturn. By December 2024, the number of insolvent individuals listed by Chinese courts as “dishonest debtors” exceeded 8.5 million, a growth of nearly 48% from four years ago and accounting for about 1% of the total workforce.

Solutions

Boosting domestic consumption is not merely a policy imperative for China — it represents a comprehensive societal transformation.

China must overhaul its fiscal system to increase public revenues and realign local government incentives. Key steps include tax reforms, increased borrowing, and the sale of state-owned enterprise (SOE) assets. Monetary policy also plays a critical role. The People’s Bank of China has already reduced the reserve requirement ratio to inject liquidity and support key sectors such as real estate, technology, green industries, consumption, and small enterprises. Further interest rate cuts are needed to spur economic activity.

SOEs and the state financial system currently skew wealth and credit toward industry and investment, limiting household income and consumption. Reforming SOE governance and addressing financial distortions is essential. Broader household participation through shareholding and dividend redistribution could redirect resources toward consumers and stimulate spending.

Increasing household income is critical to boosting consumption. This involves encouraging higher wages, labor market reforms, and support for unionization. Promoting high-value industries like technology and healthcare can create better-paying jobs. Additionally, targeted tax cuts and deductions for middle- and lower income households would enhance disposable income.

China must also reduce precautionary savings by enhancing public services and the management of unemployment risks. This includes expanding healthcare, pensions, and education — especially in rural and underserved areas. These changes require increased fiscal spending and restructuring local government incentives to prioritize social investment over infrastructure. Pilot programs such as universal basic income in select regions could serve as experimental models for reducing economic insecurity and encouraging spending.

Boosting domestic consumption in China requires a coordinated, multidimensional approach. It involves reforming institutions, reshaping incentives, empowering households, and promoting inclusive growth. With strategic foresight, strong policy action, and collaborative effort across society, China can build a resilient, consumption-driven economy that ensures long-term prosperity and stability for the country and for the world.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Chen Gang

Dr. Chen Gang is Deputy Director and Senior Research Fellow of the East Asian Institute (EAI), National University of Singapore. Since he joined the EAI in 2007, he has been tracing China’s politics, foreign policy, environmental and energy policies and publishing extensively on these issues.

Have any feedback on this article?

Related Articles