Published 14 January 2025

With its traditional economic engines sputtering, Beijing has pivoted its export machine sharply toward manufacturing to maintain growth. Colossal Chinese overcapacity is now inimical to most of the rest of the world's industrial ambitions, not least in ASEAN. Southeast Asia is experiencing its version of a 'China Shock', even as it faces a new threat of more Trump tariffs.

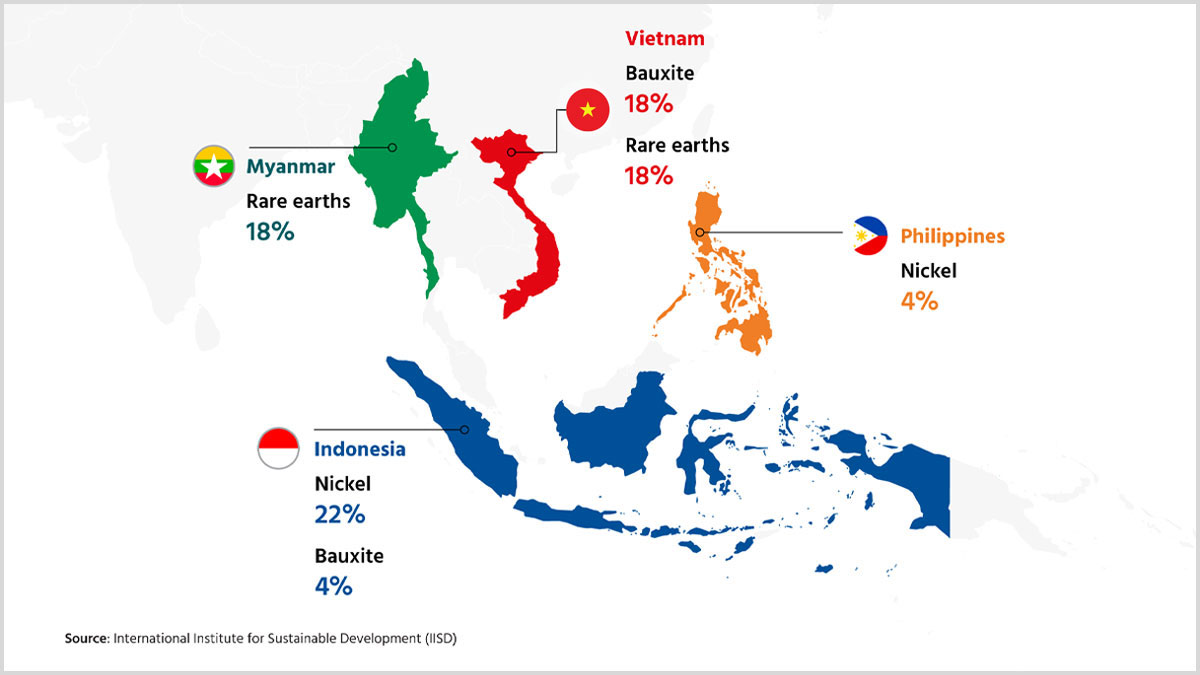

From a certain perspective, Southeast Asia’s demographics and geoeconomic assets make it the prime beneficiary of US-China trade tensions. The region’s proximity to China, availability of resources, largely neutral geopolitical positions, and integration into global value chains give it natural advantages for a promising economic future. Over the last decade, the average economic growth among the 10 member states of the Association of Southeast Asian Nations (ASEAN) has been humming along at an annual rate of around 4%.

On a closer look, however, this sanguine view threatens to be mugged by several realities buffeting the region.

The first is an ironic one. China, whose rising tide for long lifted the Southeast Asian boats in its wake, now might be turning into something of a trade liability. Free trade agreements like the Regional Comprehensive Economic Partnership (RCEP) were meant to give ASEAN’s low-cost manufacturers access to China’s vast market. Instead, with a collapsing property sector and slowing economy, Beijing has made a strategic decision to marshal ever more resources into ramping up exports – a sharply rising portion of which is entering ASEAN markets – rather than taking meaningful steps to lift its anemic domestic consumption. The result has been a growing trade surplus with ASEAN and a slew of factory closures in the region, ranging from Indonesian textile mills to Thai plastics plants.

Download ASEAN faces China Shock and Trump 2.0 by Henry Storey:

The second, of course, is the re-election of Donald Trump. For all the spillover effects of the US-China global contest, the US market has by and large remained open, allowing ASEAN to even overtake China as the largest exporter to America toward the end of the Biden administration. Trump’s mercantilist fixation on trade deficits, however, has caused a frisson of anxiety in ASEAN. This is hardly surprising given that all major ASEAN economies, except Singapore, have a robust trade surplus with the US – an indicator which Trumponomics reads as an imbalance that needs to be corrected.

The convergence of these two forces could prove particularly deleterious to ASEAN’s manufacturing sector. Direct US tariffs on ASEAN exports will complicate the business case for companies diversifying out of China. Facing even higher tariffs walls in the US, Chinese manufacturers will divert shipments to markets like ASEAN. The result could even be, in extremis, ASEAN’s premature deindustrialization.

But this outcome is by no means a foregone conclusion, writes Henry Storey, Senior Analyst at Melbourne-based political risk consultancy Dragoman. Individual ASEAN states may ride the economic opportunity well. ASEAN states each have their own agency and policy options, including defensive trade measures. But this will require adroit and proactive diplomacy as well as judicious management of competing domestic interests.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Henry Storey

Henry Storey is a senior analyst at Dragoman, a Melbourne-based political risk consultancy. He is also a regular contributor of The Interpreter published by The Lowy Institute.

Have any feedback on this article?