Trade distortion and protectionism

UNCTAD Global Trade Update March 2025

Published 01 April 2025

UN Trade and Development (UNCTAD) publishes a quarterly report providing fundamental data and analysis of global trade flows for goods and services. This report, in addition to providing trade trends and the outlook for 2025, also includes a comprehensive discussion on the role of tariffs in international trade.

Here’s how to use the UNCTAD Global Trade Update March 2025.

Why is the UNCTAD Global Trade Update March 2025 important?

With drastic trade policy shifts in the United States, including adoption of high levels of tariffs across goods and trading partners, and triggering retaliatory tariffs, the global trading system is in period of considerable change. This report on the role of tariffs in international trade highlights the impact of tariffs in place before these changes, which economies impose and face the highest tariff levels, and how tariffs can have an impact on economic development. It provides important context and information at a time when tariff imposition is poised to reshape global trade flows and value chains.

What’s in the UNCTAD Global Trade Update March 2025?

The UNCTAD Global Trade Update March 2025 is divided into two distinct sections: Policy insights on the role of tariffs in international trade, and the usual Global trade update section, with each of these two sections incorporating six sub-sections.

The report includes two principal sections:

Section 1: Policy insights on the role of tariffs in international trade

Introduction

- While global trends show a general decline in tariff rates due to trade liberalization, developing country exports face comparatively higher tariffs; tariffs have an important role for developing economies in:

- Serving as a source of government revenue;

- Acting as a policy instrument to support nascent industries; and

- Influencing market access and trade negotiations.

Advanced economies impose high tariffs on certain imports from developing economies, restricting their ability to expand exports and integrate into global value chains. (p. 2)

- High tariffs increase costs for consumers, stifling economic growth and competitiveness; developing countries must strike a balance between leveraging tariffs for economic development and integrating into the global economy through trade liberalization. (p. 2)

Tariffs by sector

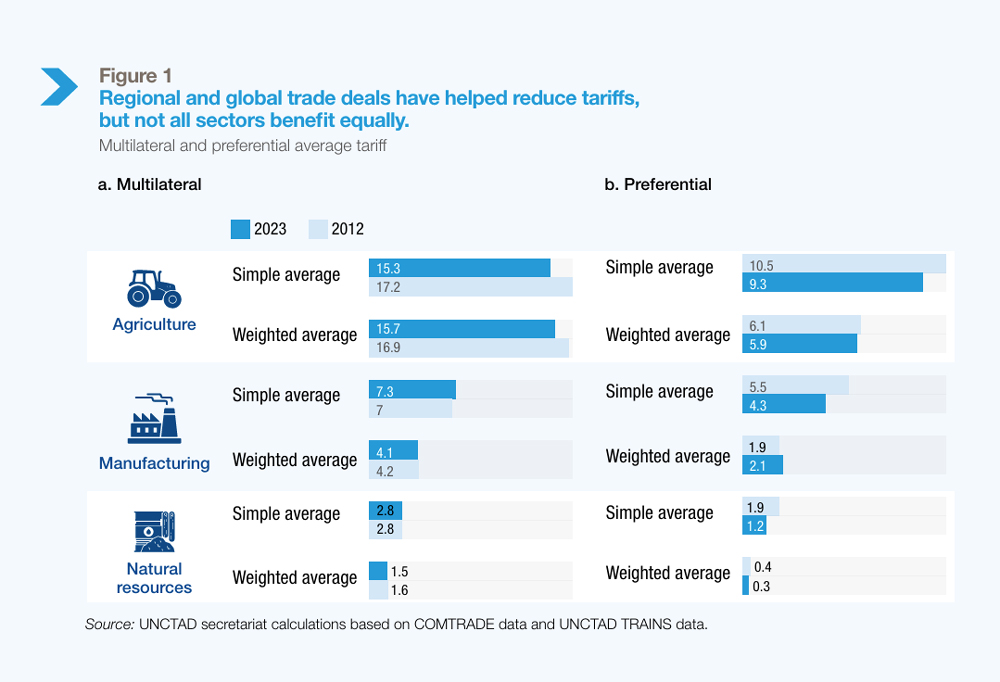

- Agriculture is highly protected in many countries, with agricultural products facing some of the highest tariffs in international trade; processed agricultural goods face higher tariffs than raw commodities, which discourages value addition in developing countries. (pp. 3-5, Figures 1-2)

- Manufactured goods experience varying tariff structures depending on the product category and region applying tariffs; manufacturing tariffs only remain high in South Asia and Africa; developed countries have the lowest tariffs on manufactures. (pp. 3-5, Figures 1-2)

- Raw materials face the lowest tariff rates among all sectors, reflecting their essential role in industrial production and global supply chains. (pp. 3-5, Figures 1-2)

Tariffs by region

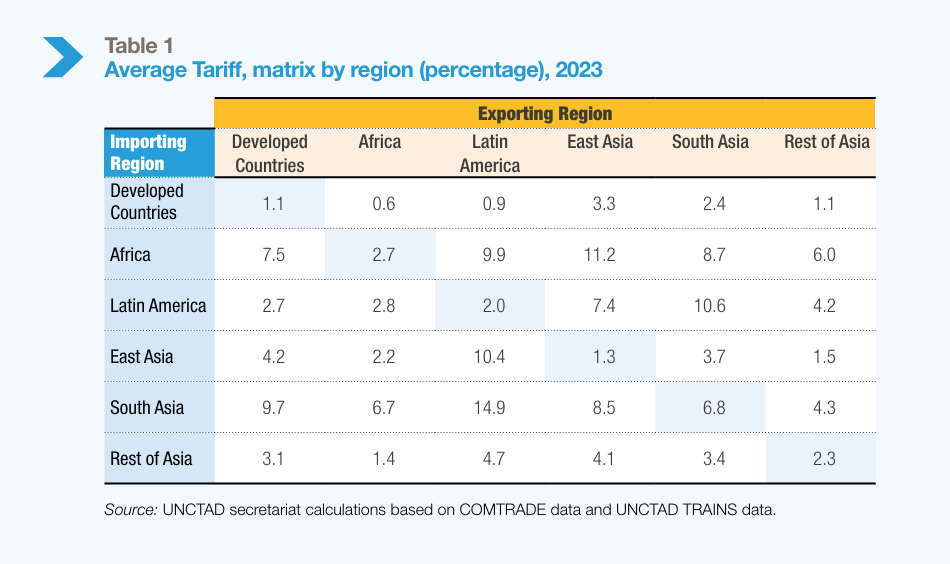

- Tariffs vary significantly across regions; developing countries both impose higher import tariffs than developed economies and face higher tariffs on their exports. (pp. 6-7, Figure 3)

- Africa and South Asia impose some of the highest import tariffs, while Latin America imposes significant tariffs; East Asia has significantly lower tariffs due to extensive trade agreements and deep economic integration; developed economies have the lowest tariffs due to multilateral agreements and focus on exporting manufactured goods. (pp. 6-8, Figure 3, Table 1)

- While South Asian and Latin American exports face higher tariffs, other regions face generally lower tariffs on exports, largely due to trade agreements, exports of natural resources and raw materials, and integration into global supply chains. (pp. 6-8, Figure 3, Table 1)

- Countries trading within their own regions face lower tariffs due to regional trade agreements while trade between regions encounters higher tariffs; South-South trade between developing countries face high tariff levels which have not changed over the past decade. (p. 7)

- Developing countries benefit from lower tariffs within regional trade blocs but face high tariff barriers when seeking to export outside of their regions, facing a competitive disadvantage compared to regional trading partners that are part of regional preferential trade agreements; East Asian exporters face fewer trade barriers globally as their exports are concentrated in industries with lower tariff rates, though East Asia’s trade competitiveness is driven by efficiency, production networks, and technological capabilities rather than high preferential margins. (p. 8)

Tariffs liberalization

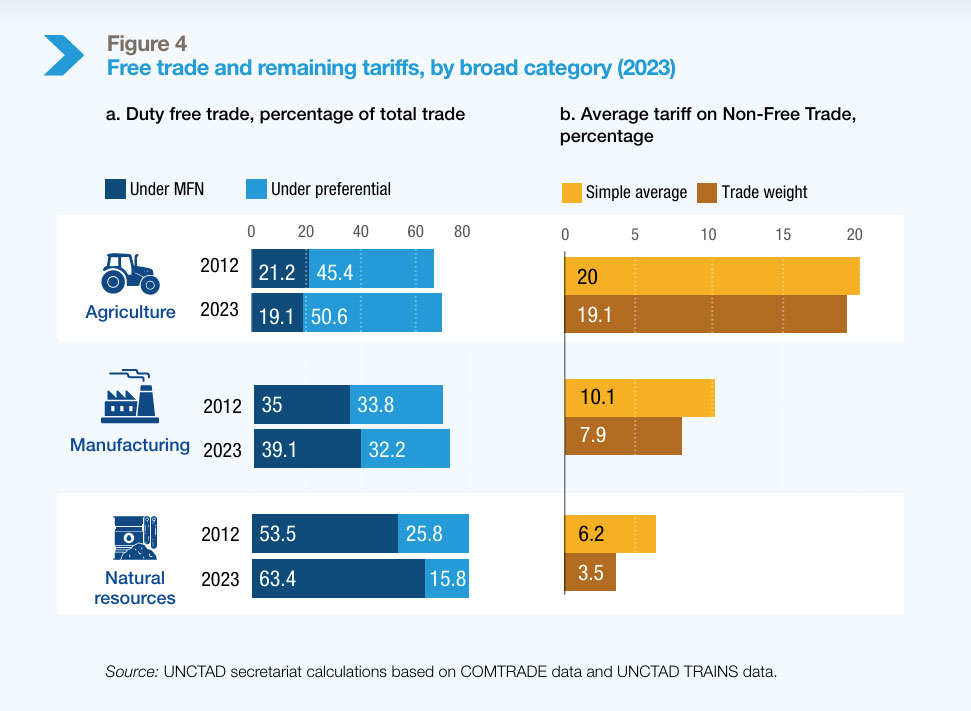

- The rules-based trading system has gradually and continuously reduced tariffs, bolstering international trade; about two-thirds of international trade occurs tariff-free, though tariff levels on the remainder can be very high. (p. 9, Figure 4)

Tariffs peaks

- Tariff peaks arise when specific goods, often in sensitive industries, are subject to significantly higher tariffs than the average to protect domestic industries from foreign competition; tariff peaks are used by developing countries and tend to concentrate in products of interest to low-income countries, including agriculture, apparel, textiles, and tanning. (pp. 10-11, Figure 5)

Tariffs escalation

- Tariff escalation means applying higher tariffs on finished consumer goods than on raw materials or intermediate inputs, a practice common in many countries to protect domestic industries that process and manufacture consumer goods; tariff escalation is more pronounced in manufacturing sectors than agriculture. (pp. 12-13, Figure 6)

- Tariff escalation harms developing countries by disincentivizing value-added processing, reducing export competitiveness and making it harder to integrate into global supply chains; developing countries can use tariff escalation as a point of negotiation in trade agreements, to encourage export diversification by shifting focus toward regional markets and support the development of regional value chains; tariff escalation shapes global trade by influencing where value-added processing takes place. (pp. 12-13, Figure 6)

Tariffs by sector

- Bound tariffs are the maximum tariff rates a country can impose under WTO rules; bound rates provide certainty and predictability, enabling businesses to plan their investment and trade operations with greater confidence and reduced risk of sudden cost increases and prevent excessive protectionism. (pp. 14-15, Figure 7)

- Many nations maintain MFN tariff rates below the bound level, providing flexibility for potential increases; “tariff water” is the difference between the applied MFN rates and the bound rates; with preferential trade agreements, the true tariff water may be less, meaning that preferential trade agreements ensure even greater stability and predictability. (pp. 14-15, Figure 7)

Section 2: Global trade update

Global trade trends and nowcast

- Global trade in goods and services saw significant growth during 2024, increasing by 3.7%; growth trajectories slowed in 2H 2024; global trade expanded by almost US$1.2 trillion in 2024, reaching US$33 trillion, a 2% rise in goods trade and a 9% rise in services trade; prices for traded goods saw no increase during Q4 2024, implying that volatile and deflationary trends observed previously have run their course. (p. 17)

Summary outlook

- Over the past four quarters, trade growth in developing countries outpaced that of developed countries, with South-South trade performing above average; in Q4 2024, growth in goods trade decelerated while trade in services maintained strong momentum; preliminary Q1 2025 data indicates continued growth in both goods and services but this may be in part from anticipated US tariffs causing shipments to be frontloaded. (p. 17)

- In 2025, international trade may shift significantly with forecasts marked by uncertainty with a risk of downturn; shifts in US trade policy, concerns over global trade imbalances, and continuing geopolitical challenges may negatively influence global trade growth; the possibility of trade policy escalations casts uncertainty over the global trade outlook, though expected easing in global inflation and China’s 2025 economic stimulus may help global trade. (p. 18)

- Trade trends for 2025 are uncertain given 1) shifts in trade policy toward protectionism and linking trade measures with non-trade policy objectives; 2) potential spillovers from ongoing trade tensions among major economies, creating a cycle of escalating trade barriers which may eventually involve third parties; 3) increases in subsidies and inward-looking industrial policy; and 4) potential for an economic slowdown in the coming quarters. (p. 18)

Trade trends in the major economies

- Q4 2024 merchandise trade was mixed among major economies; China and India trade increased, particularly in exports; South Korea’s export growth decelerated; US import growth was positive but export growth was negative; import growth was negative for Japan, Russia, the EU, and South Africa. (p. 19)

- Services trade continued to grow in Q4 2024, though at a slower pace compared to annual figures suggesting that the growth trend has plateaued in most economies; growth remained strong in Q4 for India and South Africa. (p. 19)

Regional trade trends

- Q4 2024 trade growth in developing countries grew by 2%, outpacing developed countries whose trade in imports and exports declined by 2%; South-South trade was notably stronger in Q4; most regions experienced positive overall trade growth during Q4 except for Europe and Central Asia where trade contracted. (p. 20)

Global trade imbalances

- Global imbalances in goods trade increased in 2024, with the US showing the largest trade deficit and China the largest surplus; the EU recorded a significant trade surplus in 2024 due to high energy prices; bilateral imbalances in goods trade among major economies remain high and have mostly increased over the last quarter. (p. 21)

Global trade dynamics and trade dependence

- Rises in global friendshoring and trade concentration trends in 2023 reversed in 2024, signaling a shift away from dynamics favoring trade between geopolitically close countries; trade concentration is now below 2021 levels, suggesting a global trade structure where smaller countries play a larger role; nearshoring has also declined in recent quarters, suggesting a resurgence of trade between geographically distant countries; geoeconomic issues and restructuring of value chains play a significant role in shaping key bilateral trade trends. (p. 22)

Global trade trends at the sectoral level

- Trade growth has varied significantly across sectors over the past four quarters, with growth in Q4 most pronounced in agri-food, communication equipment, precision instruments, and transport, and declining in the apparel sector and extractive industries. (p. 23)

How to apply the insights

-

This report is useful to policymakers and analysts for understanding the current state of play in global trade, whose export and import growth is growing or decelerating, and what regions or countries are engaging or re-orienting trade flows.

-

The quarterly series provides a useful ongoing summary to keep track of trade trends.

Conclusion

The UNCTAD Global Trade Update March 2025 introduces a helpful overview of the use of tariffs, combined with current trade flows and trends, at a time when trade policy is seeing significant shifts and provides highly relevant context for better understanding one of the most important economic topics in the news today.

Complementary reports and analysis

Hinrich Foundation

- The looming chaos of Trump’s trade "Liberation Day"

- Trump’s "reciprocal" tariffs took root in the WTO's failings

- Regional cooperation can buffer global value chains against uncertainty

External Resources

- World Tariff Profiles 2024 – WTO, the International Trade Centre and UNCTAD

Information on tariffs and non-tariff measures imposed by over 170 countries and customs territories. - WTO Tariff & Trade Data Integrated Database and Consolidated Tariff Schedules – World Trade Organization

A comprehensive database of tariff schedules. - OECD Economic Outlook, Interim Report March 2025 – OECD

A periodic report on prospects for the global economy and analysis of economic growth over the previous year.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).